If you have ever looked at a commercial property listing and seen “8% Cap” written next to the price, you probably wondered what it means and whether it is good or bad. Well, the cap rate is one of the most important numbers in commercial real estate investing. It tells you how much money a property can make compared to what it costs. Once you understand it, buying and comparing properties becomes so much simpler.

What Exactly Is a Cap Rate?

A cap rate, short for capitalization rate, is a percentage that shows the expected yearly return on a commercial property. It compares the money a property earns to its market value or purchase price.

Think of it this way. If you buy a property for $1,000,000 and it earns $80,000 a year after paying its bills, your cap rate is 8%. That means you are getting 8% of your money back each year, assuming you paid all cash with no loan.

Jonathan Squires, managing director at Cushman and Wakefield, puts it simply: a cap rate expresses the expected annual return on an investment property. It does not matter what the property looks like or where it is; the cap rate lets you compare any two properties side by side, which is why investors love it so much.

Why Does Cap Rate Matter in Commercial Real Estate?

Honestly, when I first started learning about commercial real estate, I was confused by all the numbers. Price per square foot, vacancy rates, lease terms. But the capitalization rate stood out because it gives you one clean number to compare properties, even if they are in completely different cities or different property types.

It matters because commercial property value is not based on what your neighbor’s building sold for. It is based on income. The more income a property produces, the more it is worth. The cap rate is the tool that connects those two things. It helps investors understand both the risk profile and the return on investment at a glance.

How to Calculate the Cap Rate: The Simple Formula

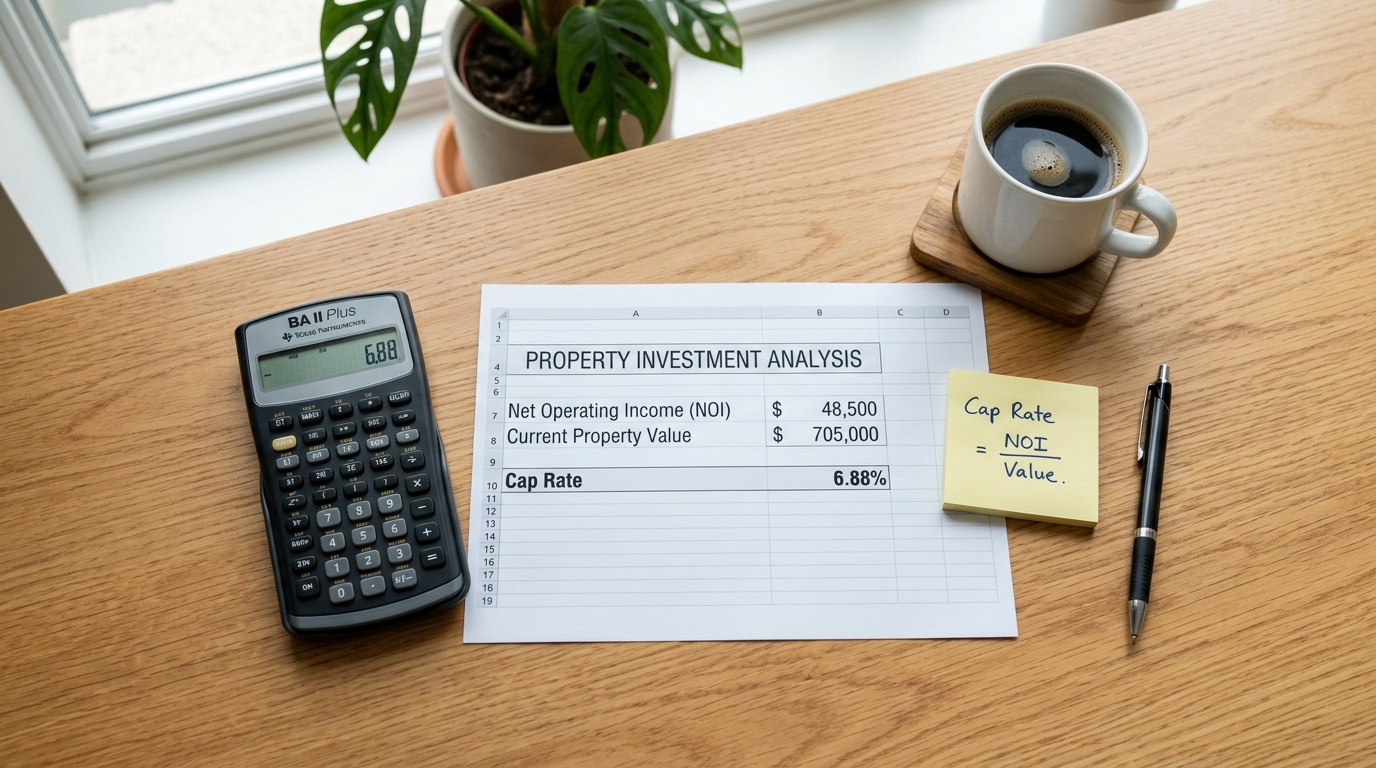

The formula for cap rate is short and simple. You just need two numbers: the property’s net operating income and its current market value.

Cap Rate = Net Operating Income (NOI) / Current Market Value x 100

That is it. Nothing more. If a property earns $500,000 a year after expenses and is worth $5,000,000, the cap rate is 10%. You can also flip this formula to find the property’s value if you know the NOI and the going cap rate in that market.

Cap Rate Calculation Example (Step by Step)

Let me walk you through a real example so it sticks.

Say you are looking at a small retail building. It brings in $120,000 a year in rent. After paying property taxes, insurance, repairs, and management fees, the building’s expenses come to $30,000. So the net operating income is $120,000 minus $30,000, which equals $90,000.

The seller is asking $1,200,000. You divide $90,000 by $1,200,000 and get 0.075. Multiply by 100, and you get a cap rate of 7.5%. That means you would earn 7.5% of your money back each year through the property’s income, before counting any loan or mortgage payments.

You can also work backwards. If similar properties in that market are trading at a 7% cap rate and your building earns $90,000 a year, the estimated value is $90,000 divided by 0.07, which comes to about $1,285,000. This is the basis of the income capitalization approach to property valuation, and it is how most appraisers set property values in commercial real estate.

What Goes Into Net Operating Income (NOI)?

The NOI is the heart of the cap rate formula. It is the money left over after you pay all the property’s running costs, but before you pay your mortgage or any loan.

You start with the total annual income from rent. Then you subtract the operating expenses. These include things like property taxes, insurance, maintenance, property management fees, and utilities. What is left is the NOI.

What does NOT go into the NOI? Your mortgage payments. The cap rate is designed to measure the property itself, not how you financed it. This way, two investors using different loan sizes can still compare the same property fairly. It is purely about the income-producing property and its ability to earn money on its own.

What Is a Good Cap Rate for Commercial Property?

This is the question everyone asks, and to be fair, there is no one answer. What is good depends on your goals, your risk tolerance, and the market you are buying in. That said, most investors in the US consider a cap rate between 4% and 10% to be normal for commercial property.

A lower cap rate, say 3% to 5%, usually means the property is in a top location, has strong tenants, and carries low risk. Think Class A office buildings in Manhattan or multifamily buildings in prime cities. A higher cap rate, like 8% to 12%, usually means more risk but also more potential reward.

Cap Rate Ranges by Property Type and Market

Cap rates are not the same across all property types. Here is a simple look at typical ranges based on market data:

| Property Type | Primary Markets | Secondary Markets | Tertiary Markets |

| Multifamily | 3.5% – 5.0% | 4.5% – 6.0% | 5.5% – 8.0% |

| Office | 4.0% – 6.0% | 5.5% – 7.5% | 7.0% – 9.5% |

| Retail | 4.5% – 6.5% | 6.0% – 8.0% | 7.5% – 10.0% |

| Industrial | 4.0% – 5.5% | 5.0% – 7.0% | 6.0% – 8.5% |

Source: LoopNet Cap Rate Guide, based on general US market data (2024–2025). For current market estimates, see LoopNet’s Cap Rate Explained.

Keep in mind these are general ranges. The actual cap rate for a specific property depends on many things, including the quality of tenants, the length of leases, and local supply and demand.

High Cap Rate vs. Low Cap Rate: What Does It Mean for You?

Here is a way to think about it. Cap rates and property prices move in opposite directions. When cap rates go up, property prices tend to go down. When cap rates fall, prices rise. This inverse relationship is one of the most important things to understand in commercial real estate investing.

A low cap rate means you are paying more for each dollar of income. That might be fine if the property is stable, well-located, and low risk. Think of it like buying a government bond. You get a safe return, but not a huge one.

A high cap rate means you are paying less per dollar of income, but there is usually a reason. Maybe the area is riskier, the tenants are weaker, the building needs work, or there is high vacancy. Most people think a high cap rate is always better. But from what I have seen, that is not always true. A 10% cap rate on a struggling building in a declining market can be far worse than a 5% cap rate on a solid building with long-term credit tenants in a growing city.

Key Factors That Affect Cap Rates

Cap rates do not exist in a vacuum. They move based on what is happening in the economy, the property itself, and the local real estate market. Knowing these factors helps you read the market better and avoid overpaying.

How Interest Rates, Location, and Lease Terms Change Cap Rates

One of the biggest drivers of cap rates is interest rates. When borrowing becomes more expensive, investors expect higher returns to make a deal worthwhile. That pushes cap rates up. When interest rates fall, investors accept lower cap rates because their borrowing costs drop too.

Location matters a lot. A property in a strong primary market like New York or Los Angeles will have a much lower cap rate than a similar building in a small city. This reflects lower risk, higher demand, and better supply and demand conditions.

Lease terms also play a big role. A building with long-term leases signed by strong national tenants, what investors call credit tenants, carries very low risk. The income is predictable. So investors accept a lower cap rate. A building with short leases or month-to-month tenants is riskier. Cap rates will be higher to reflect that uncertainty.

Other factors that move cap rates include local vacancy rates, property condition, zoning rules, the creditworthiness of tenants, and even the general economic outlook, including GDP growth and unemployment levels.

Cap Rate Trends in 2025: What CBRE Data Shows

The good news for investors in 2025 is that cap rates appear to be stabilizing after a period of rising rates. According to a study published by CBRE in their H2 2025 Cap Rate Survey, the all-property cap rate held steady throughout the second half of 2025, and total commercial real estate transaction volume rose by approximately 19%. Pricing has stabilized with several key price indices no longer declining. This suggests the market may be entering a new cycle.

The survey, based on around 3,600 cap rate estimates from over 200 CBRE capital markets professionals across more than 50 US markets, also showed that nearly 50% of respondents expect retail, industrial, and hotel cap rates to begin declining in the near term. According to CBRE, multifamily remains the top choice for investors, followed by industrial. You can read the full findings at CBRE’s H2 2025 Cap Rate Survey.

For investors, this means deals may become more competitive again. Getting a clear picture of cap rates now, before compression kicks in, could give you an edge.

Limitations of Cap Rate: What It Cannot Tell You

Cap rate is a powerful tool, but it is not perfect. Honestly, I have seen investors make expensive mistakes by relying on the cap rate alone. It is a starting point, not a finish line.

Why You Should Not Use Cap Rate Alone

The cap rate has a few important blind spots. First, it ignores debt and financing. It assumes you are buying the property in cash with no mortgage. In the real world, most investors use loans. A property with a 7% cap rate might still be a bad deal if interest rates on your loan are at 7.5%, because you would be losing money from day one.

Second, the cap rate only looks at current income. It does not account for future rent increases, lease renewals, upcoming vacancies, or any renovations you might need to make. A building with great current tenants might look solid today, but become risky when those leases expire next year.

Third, it does not measure the full return over time. If you renovate a building and raise rents, the cap rate improves. But the cap rate at the time of purchase did not tell you about that opportunity. This is where understanding the business plan and the market matters just as much as the numbers.

Better Metrics to Use Alongside Cap Rate

The Internal Rate of Return (IRR), sometimes called the Levered IRR, is a better metric for deeper analysis because it includes the effect of debt, future income changes, and your eventual sale price. It gives you the full picture over your entire holding period.

Cash-on-cash return is another useful number. It measures how much cash you earn each year compared to how much cash you actually put in, including your down payment and loan costs. It is much more practical for investors who are using financing.

Most experienced investors use the cap rate as a quick first filter. It helps you decide in seconds whether a property is even worth looking at. Once it passes that test, you dig deeper with IRR, cash-on-cash return, vacancy projections, and a full due diligence review.

Conclusion

Understanding the cap rate of commercial property can change how you look at every listing you see. It is a fast, clean way to measure expected return and compare properties, no matter where they are or what type they are.

The key things to remember: cap rate equals NOI divided by market value. A lower cap rate means lower risk and a higher price. A higher cap rate means more risk and more potential reward. Always use it as a starting tool, not your only tool. Combine it with IRR, cash-on-cash return, and solid research on the local market.

The commercial real estate world is full of numbers, but cap rate is one of the first you should master. Once you do, deals start making a lot more sense. I hope this guide made it easier for you. If you have questions or want to share your own experience with cap rates, I would love to hear from you in the comments below.

Frequently Asked Questions

1. What is a cap rate in simple words?

A cap rate is a percentage that shows how much money a commercial property earns each year compared to its price. For example, if a building costs $1,000,000 and earns $80,000 a year after expenses, the cap rate is 8%. It helps investors quickly compare different properties and understand the expected return on investment<span style=”font-weight: 400;”>.

2. What is a good cap rate for commercial property in 2025?

Most US investors consider a cap rate between 4% and 10% to be normal. A cap rate of 4% to 6% is typical for safe, well-located properties in strong markets. A cap rate of 7% to 10% or higher usually means more risk. According to CBRE’s H2 2025 Cap Rate Survey, cap rates have stabilized across most property types, with multifamily and industrial showing the lowest rates in major markets.

3. Does a higher cap rate mean a better investment?

Not always. A higher cap rate means a higher expected return, but it also usually means more risk. The property might have vacancy issues, weak tenants, or be in a less stable market. A lower cap rate on a solid property in a growing city can sometimes be a much safer and smarter investment than a high cap rate on a troubled building. Always look beyond the number.

4. Does the cap rate include mortgage payments?

No. The cap rate formula does not include mortgage or loan payments. It is based on net operating income, which is the income before any debt service. This makes it a clean, unbiased way to compare properties regardless of how each investor plans to finance the purchase. For analysis that includes financing, use the cash-on-cash return or the Internal Rate of Return instead.

5. How does location affect the cap rate?

Location has a huge effect on cap rates. Properties in large, high-demand cities like New York or Los Angeles tend to have lower cap rates because they are seen as safer, more stable investments. Properties in smaller or less popular markets tend to have higher cap rates because there is more risk. The same type of building, like a multifamily apartment block, can have a 4% cap rate in a primary market and a 7% cap rate in a smaller city. Always compare properties within the same market for a fair picture.